Building a strong credit score in the USA can make your financial life easier. A good credit score may help you qualify for better credit cards, lower loan interest rates, apartment approvals, car financing, mortgage options, and even better insurance pricing in some states.

But here is the important truth: you cannot build excellent credit overnight. Credit scoring is based on real financial behavior over time. However, you can improve your credit score faster by focusing on the actions that matter most: paying on time, lowering credit utilization, fixing credit report errors, keeping old accounts open, and using credit responsibly.

This guide explains how working professionals in the USA can build credit score fast using practical, legal, and AdSense-friendly strategies.

Disclaimer: This article is for educational purposes only. Income, results, and earnings may vary based on skills, effort, market demand, experience, and consistency. This is not financial advice.

Affiliate Disclosure: Some links mentioned in this article may be affiliate links. If you purchase through these links, the website may earn a small commission at no extra cost to you.

What Is a Credit Score?

A credit score is a three-digit number that helps lenders estimate how likely you are to repay borrowed money. In the USA, most credit scores range from 300 to 850.

A higher score usually shows lower credit risk. A lower score may make it harder to qualify for loans, credit cards, apartments, or favorable interest rates.

The most commonly used credit scoring model is the FICO Score, although lenders may also use VantageScore or other internal scoring systems.

General Credit Score Ranges

| Credit Score Range | General Meaning |

|---|---|

| 300–579 | Poor |

| 580–669 | Fair |

| 670–739 | Good |

| 740–799 | Very Good |

| 800–850 | Excellent |

These ranges are general. Different lenders may use different approval rules.

How Credit Scores Are Calculated

To build your credit score fast, you must understand what affects it.

FICO scores are generally based on five major categories: payment history, amounts owed, length of credit history, credit mix, and new credit. Payment history is usually the largest factor at 35%, followed by amounts owed at 30%, length of credit history at 15%, credit mix at 10%, and new credit at 10%.

| Credit Score Factor | Approximate Weight | What It Means |

|---|---|---|

| Payment history | 35% | Whether you pay bills on time |

| Amounts owed / utilization | 30% | How much available credit you use |

| Length of credit history | 15% | Age of your credit accounts |

| Credit mix | 10% | Variety of credit types |

| New credit | 10% | Recent applications and new accounts |

The fastest improvement usually comes from two areas: payment history and credit utilization.

Can You Build Credit Score Fast in USA ?

Yes, but “fast” has limits.

Some actions can affect your score within a few weeks or months, especially if they change your reported credit card balances or correct inaccurate negative information. Other improvements, such as building a long payment history, take time.

Fastest Credit Score Improvement Actions

| Action | Possible Timeline | Why It Helps |

|---|---|---|

| Pay down credit card balances | 30–60 days | Lowers credit utilization |

| Dispute credit report errors | 30–45+ days | Removes inaccurate negative data if corrected |

| Become an authorized user | 30–60 days | May add positive account history |

| Set up autopay | Immediate habit improvement | Prevents late payments |

| Request a credit limit increase | 30–60 days | Can lower utilization if spending stays the same |

| Open a secured credit card | 1–3 months | Helps build payment history |

Results are not guaranteed because every credit profile is different.

Step 1: Check Your Credit Reports First

Before trying to build credit fast, check your credit reports from all three major credit bureaus:

- Equifax

- Experian

- TransUnion

You can get free weekly online credit reports from all three bureaus through AnnualCreditReport.com. The Consumer Financial Protection Bureau also says consumers can request free credit reports through AnnualCreditReport.com or by calling the official phone number.

Why this matters:

- You may find incorrect late payments.

- You may find accounts that do not belong to you.

- You may find wrong balances or limits.

- You may find old negative items that should no longer appear.

- You may detect identity theft early.

What to Review on Your Credit Report

| Report Section | What to Check |

|---|---|

| Personal information | Name, address, employer details |

| Open accounts | Balances, limits, payment status |

| Closed accounts | Accuracy and reporting dates |

| Hard inquiries | Unauthorized credit applications |

| Collections | Incorrect or outdated collection accounts |

| Public records | Bankruptcy or legal reporting accuracy |

If your report contains errors, fixing them may be one of the fastest ways to improve your credit profile.

Step 2: Dispute Credit Report Errors

If you find inaccurate information, dispute it with the credit bureau and also contact the company that reported the incorrect information.

Federal law allows consumers to dispute inaccurate information on their credit reports for free. AnnualCreditReport.com states there is no fee to file a dispute, and the CFPB recommends contacting both the credit reporting company and the company that provided the information.

Common Credit Report Errors

- A payment marked late even though it was paid on time

- An account that does not belong to you

- Incorrect balance or credit limit

- Duplicate collection account

- Incorrect account status

- Old negative information still appearing

- Identity theft-related accounts

Simple Dispute Process

- Download your credit reports.

- Highlight the inaccurate item.

- Gather proof such as statements, payment confirmations, or letters.

- File a dispute with the credit bureau.

- Contact the lender or collection agency directly.

- Keep copies of everything.

- Track the dispute result.

Important Warning

Do not dispute accurate information just to “test” the system. Accurate negative information usually cannot be legally removed just because you do not like it.

Step 3: Pay Every Bill on Time

Payment history is the biggest credit score factor. Even one late payment can hurt your score, especially if it becomes 30 days late and is reported to the credit bureaus.

For working professionals, the easiest solution is automation.

Practical Tips to Avoid Late Payments

- Set up autopay for at least the minimum payment.

- Add payment reminders on your calendar.

- Pay credit cards before the statement closing date.

- Keep one checking account dedicated to bills.

- Review all due dates once per month.

- Contact lenders early if you expect payment difficulty.

Best Practice

Use autopay for the minimum amount, then manually pay extra before the due date. This protects you from accidental late payments while still giving you control over your cash flow.

Step 4: Lower Your Credit Utilization

Credit utilization means how much of your available revolving credit you are using.

Example:

If your credit card limit is $10,000 and your balance is $3,000, your utilization is 30%.

Credit utilization is part of the “amounts owed” category, which is a major factor in FICO scoring. FICO lists amounts owed as 30% of the score calculation.

Credit Utilization Example

| Credit Limit | Reported Balance | Utilization |

|---|---|---|

| $1,000 | $900 | 90% |

| $1,000 | $500 | 50% |

| $1,000 | $300 | 30% |

| $1,000 | $100 | 10% |

Many experts suggest keeping utilization below 30%, but for faster score improvement, keeping it below 10% may be better if possible.

How to Lower Utilization Fast

- Pay down credit card balances.

- Make multiple payments during the month.

- Pay before the statement closing date.

- Request a credit limit increase.

- Avoid large purchases before applying for a loan.

- Spread balances across cards carefully, but avoid increasing total debt.

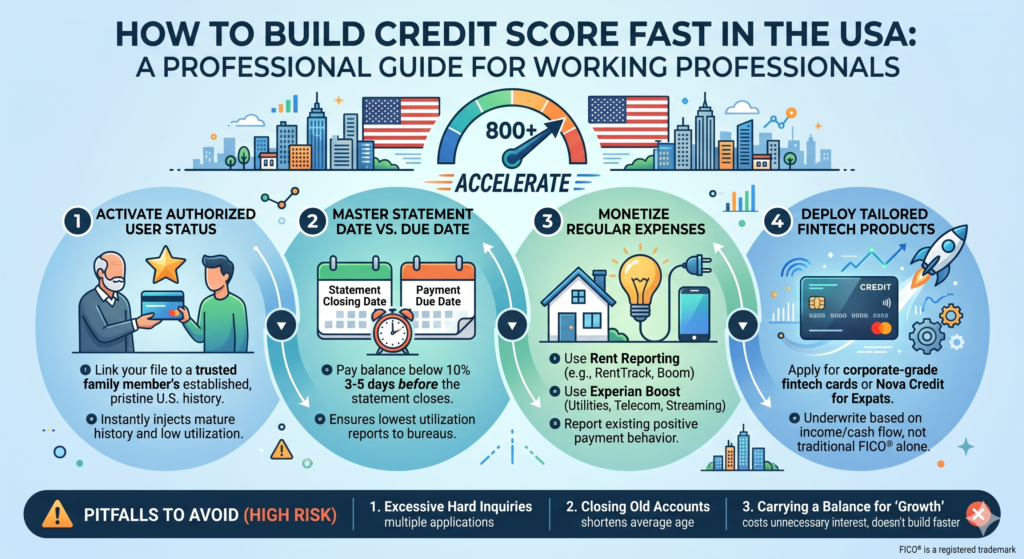

Statement Date vs Due Date

This is important.

Your credit card issuer may report your balance to the credit bureaus around the statement closing date, not necessarily after your due date. That means you can pay in full by the due date and still show high utilization if your statement balance was high.

To improve your score faster, try paying down your balance before the statement closes.

Step 5: Request a Credit Limit Increase

A credit limit increase can improve your utilization ratio if your spending stays the same.

Example:

| Situation | Credit Limit | Balance | Utilization |

|---|---|---|---|

| Before increase | $5,000 | $1,500 | 30% |

| After increase | $10,000 | $1,500 | 15% |

This can help your score because your reported utilization becomes lower.

When to Request a Credit Limit Increase

You may have a better chance if:

- You have paid on time for at least 6–12 months.

- Your income has increased.

- Your current utilization is not extremely high.

- You have no recent missed payments.

- Your account is in good standing.

Caution

Some issuers may perform a hard inquiry for a credit limit increase. Ask first. A hard inquiry may temporarily lower your score.

Step 6: Become an Authorized User

Becoming an authorized user means someone adds you to their credit card account. If the card issuer reports authorized user activity to the credit bureaus, the account may appear on your credit report.

This can help if the account has:

- Long positive history

- Low utilization

- No late payments

- Good standing

Example

If a family member has a 10-year-old credit card with a $15,000 limit, low balance, and perfect payment history, being added as an authorized user may help your credit profile.

Risk

If the primary cardholder misses payments or carries a high balance, it may hurt your score. Only use this strategy with someone financially responsible.

Step 7: Use a Secured Credit Card If You Are New to Credit

If you have no credit history or a thin credit file, a secured credit card can help.

A secured card usually requires a refundable security deposit. For example, you may deposit $200 and receive a $200 credit limit.

How to Use a Secured Card Correctly

- Use it for one small recurring expense.

- Keep utilization low.

- Pay the balance in full every month.

- Avoid cash advances.

- Monitor your statements.

- Upgrade to an unsecured card when eligible.

Good Uses

- Netflix or streaming subscription

- Gas

- Phone bill

- Small grocery purchase

The goal is not to spend more. The goal is to create positive payment history.

Step 8: Consider Credit Builder Loans Carefully

A credit builder loan is designed to help people build credit. Instead of receiving the loan amount upfront, your payments are usually held in an account and released after you complete the payment term.

This may help if you need installment loan history, but it is not always necessary.

Pros and Cons

| Pros | Cons |

|---|---|

| Can build payment history | May include fees or interest |

| Helps credit mix | Not instant |

| Useful for thin credit files | Missed payments can hurt |

| Structured monthly payments | May not be needed if you already have credit |

Before using a credit builder loan, compare costs and make sure payments are reported to all three credit bureaus.

Step 9: Keep Old Accounts Open

Length of credit history matters. Closing old credit cards can reduce your average account age and may also lower your total available credit, increasing utilization.

If an old card has no annual fee, consider keeping it open and using it occasionally for a small purchase.

When Closing a Card May Make Sense

- It has a high annual fee.

- You cannot control spending.

- The card has poor terms.

- You are simplifying finances for a reason.

Before closing, check how it may affect your utilization and account age.

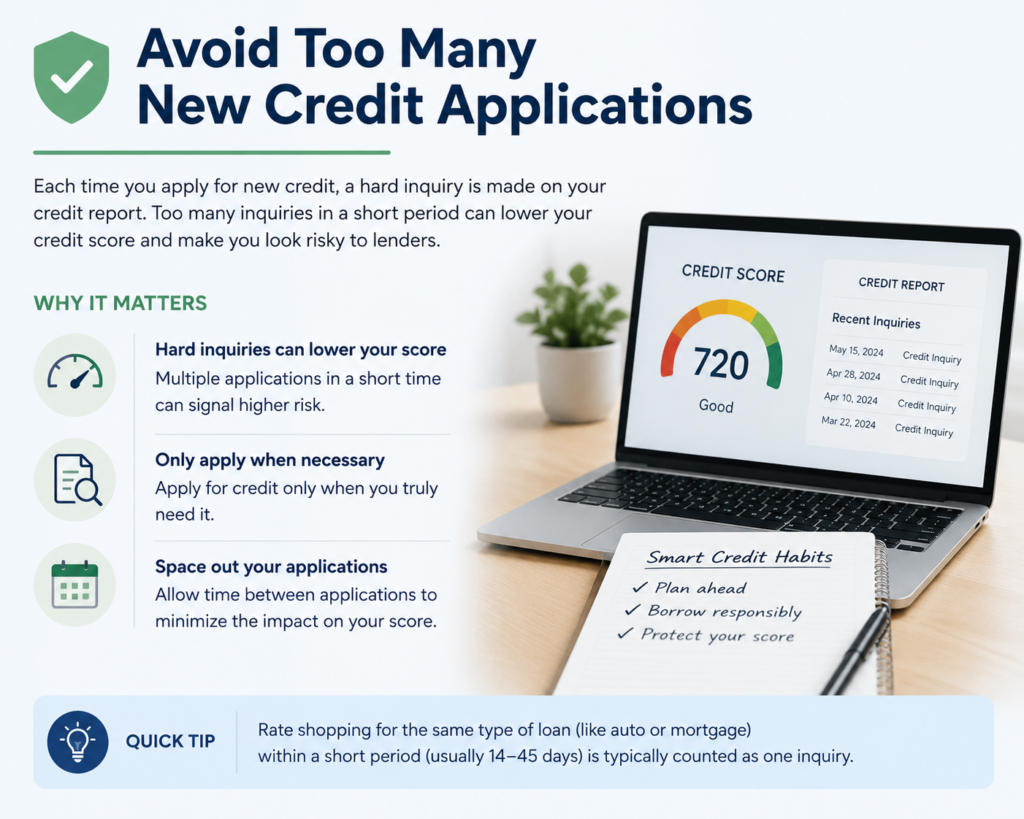

Step 10: Avoid Too Many New Credit Applications

Every time you apply for credit, the lender may perform a hard inquiry. One inquiry may have a small effect, but several applications in a short time can hurt your score and make lenders see you as higher risk.

Avoid Applying Too Often For:

- Credit cards

- Personal loans

- Store cards

- Auto loans

- Buy now, pay later plans that report credit activity

- Financing offers you do not need

If you are planning to apply for a mortgage, auto loan, or apartment, avoid unnecessary credit applications for several months beforehand.

Step 11: Handle Collections Strategically

Collection accounts can damage your credit score. If you have collections, do not ignore them.

What to Do

- Verify the debt is yours.

- Check the date and amount.

- Ask for written validation.

- Understand your state’s statute of limitations.

- Negotiate carefully if you decide to pay.

- Get agreements in writing.

- Keep records of payment.

Some newer scoring models may treat paid collections more favorably than unpaid collections, but not all lenders use the same model. So, paying a collection may or may not create a fast score increase.

If the collection is inaccurate, dispute it.

Step 12: Avoid Credit Repair Scams

Be careful with companies that promise to “erase bad credit fast” or guarantee a specific score increase.

The FTC explains that the Credit Repair Organizations Act bars credit repair companies from demanding advance payment, requires written contracts, and gives consumers cancellation rights. The FTC also warns that debt relief and credit repair scams may charge large upfront fees and fail to deliver meaningful help.

Red Flags

- Guaranteed credit score increase

- Promise to remove accurate negative items

- Upfront payment before work is completed

- Pressure to act immediately

- No written contract

- Advice to create a new identity or fake credit profile

- Claims that sound too good to be true

Safer Alternative

You can dispute inaccurate credit report information yourself for free. If you need help, consider a reputable nonprofit credit counseling agency.

Best Strategy for Working Professionals

Working professionals often have stable income but limited time. The best credit-building strategy should be simple, automated, and repeatable.

30-Day Credit Improvement Plan

| Week | Action Plan |

|---|---|

| Week 1 | Pull credit reports from all three bureaus and review errors |

| Week 2 | Dispute inaccurate items and organize payment due dates |

| Week 3 | Pay down credit card balances before statement closing dates |

| Week 4 | Set up autopay, request limit increases if appropriate, monitor progress |

90-Day Credit Improvement Plan

| Month | Focus |

|---|---|

| Month 1 | Fix errors, stop late payments, lower utilization |

| Month 2 | Build positive reporting with low balances |

| Month 3 | Review score movement, avoid new applications, maintain habits |

6-Month Credit Growth Plan

| Month | Goal |

|---|---|

| 1 | Credit report cleanup |

| 2 | Utilization below 30% |

| 3 | Utilization below 10% if possible |

| 4 | Add secured card or authorized user if needed |

| 5 | Maintain perfect payments |

| 6 | Recheck reports and optimize accounts |

Credit Score Improvement Example

Imagine a working professional named David.

David has:

- Credit score: 625

- Two credit cards

- Total credit limit: $5,000

- Total balance: $3,500

- Utilization: 70%

- No late payments

- One incorrect collection account

David takes these actions:

- Pays balances down from $3,500 to $1,000.

- Lowers utilization from 70% to 20%.

- Disputes the incorrect collection account.

- Sets autopay for all accounts.

- Stops applying for new credit.

Within a few months, David may see meaningful improvement because he fixed two major issues: high utilization and inaccurate negative reporting.

This is not guaranteed, but it shows how targeted actions can work faster than random credit hacks.

Beginner Mistakes to Avoid

1. Paying Only After the Statement Reports

If your statement reports a high balance, your utilization may look high even if you pay in full later. Pay before the statement closing date when possible.

2. Closing Old Credit Cards Too Soon

Closing old accounts can reduce available credit and shorten your credit history.

3. Applying for Too Many Cards

Multiple hard inquiries can hurt your score and make you look risky to lenders.

4. Believing Guaranteed Credit Repair Claims

No legal company can guarantee removal of accurate negative information.

5. Ignoring Small Bills

Medical bills, utilities, subscriptions, and old accounts can become collections if ignored.

6. Carrying a Balance to Build Credit

You do not need to pay interest to build credit. Paying in full is usually better.

7. Using Buy Now, Pay Later Without Tracking It

Buy now, pay later services can make spending feel smaller than it is. Some BNPL activity may affect credit reporting depending on the provider and scoring model, so track all obligations carefully.

Best Tools and Services That May Help

Affiliate-friendly mentions can fit naturally in this topic, but they should be presented honestly.

Useful tools may include:

- Credit monitoring apps

- Budgeting apps

- Secured credit cards

- Credit builder accounts

- Bank account alerts

- Identity theft monitoring

- Bill payment reminder tools

What to Look For

| Tool Type | Useful Feature |

|---|---|

| Credit monitoring app | Alerts for score/report changes |

| Budgeting app | Helps control spending and debt payoff |

| Secured credit card | Builds payment history |

| Identity monitoring | Alerts for suspicious activity |

| Bill reminder app | Prevents missed payments |

Do not recommend a product only because it pays commission. Recommend it only if it genuinely helps the reader.

How Long Does It Take to Build Credit?

The timeline depends on your starting point.

| Starting Situation | Possible Timeline |

|---|---|

| No credit history | 3–6 months to generate a score |

| High utilization only | 30–60 days after balances report lower |

| One recent late payment | Several months to years for full recovery |

| Credit report errors | 30–45+ days if corrected |

| Thin credit file | 6–12 months of positive history |

| Serious negative history | 12–24+ months or longer |

The fastest improvements usually happen when you reduce high balances or correct inaccurate negative information.

Advanced Credit Optimization Tips

For expert-level readers and working professionals, here are more advanced strategies.

Use the AZEO Method

AZEO means “All Zero Except One.” This strategy means all credit cards report a zero balance except one card, which reports a small balance.

This may help optimize utilization before a major loan application. It is not necessary for everyone, but it can be useful before applying for a mortgage or auto loan.

Track Statement Closing Dates

Your due date and statement closing date are different. Track both. Paying before the closing date can reduce reported utilization.

Separate Personal and Business Credit

If you are self-employed or have a side business, consider building business credit separately. This may help protect personal utilization, depending on the products used.

Avoid Financing Before Major Applications

Before applying for a mortgage or auto loan, avoid opening new cards, personal loans, or unnecessary financing plans.

Keep Utilization Low Across Each Card

Overall utilization matters, but high utilization on one individual card may also affect scoring. Try to keep each card’s balance low.

Final Checklist to Build Credit Score Fast

Use this checklist:

- Check all three credit reports.

- Dispute inaccurate information.

- Pay every bill on time.

- Set up autopay.

- Lower credit card utilization.

- Pay before statement closing dates.

- Request credit limit increases carefully.

- Keep old no-fee accounts open.

- Avoid unnecessary hard inquiries.

- Use secured credit if you have no credit.

- Avoid credit repair scams.

- Monitor your progress monthly.

Conclusion

Building credit score fast in the USA is possible when you focus on the highest-impact actions. For most working professionals, the best strategy is simple: pay on time, reduce credit utilization, correct report errors, avoid unnecessary applications, and build a long record of responsible credit use.

There are no legal shortcuts that guarantee instant results. But if you take the right steps consistently, your credit profile can become stronger over time. A better credit score can help you access better financial opportunities, lower borrowing costs, and more flexibility in your personal and professional life.

FAQ: How to Build Credit Score Fast in USA

1. What is the fastest way to improve credit score in the USA?

The fastest ways are usually paying down credit card balances, reducing utilization, disputing inaccurate credit report errors, and making sure all payments are on time.

2. Can I build credit in 30 days?

You may see some improvement in 30 days if your lower balances or corrected errors are reported quickly. However, building strong credit usually takes several months or longer.

3. Does paying rent build credit?

Rent payments may help if they are reported to the credit bureaus through a rent reporting service. Not all landlords or services report rent payments.

4. Is a secured credit card good for building credit?

Yes, a secured credit card can help build credit if it reports to the major credit bureaus and you pay on time every month.

5. Should I carry a balance to build credit?

No. You do not need to carry a balance or pay interest to build credit. Paying in full and on time is usually better.

6. How much credit utilization is good?

Below 30% is commonly recommended, but below 10% may be better for score optimization if possible.

7. Do credit repair companies really work?

Some may help with paperwork, but they cannot legally remove accurate negative information. Be careful with companies that demand upfront fees or guarantee results.

8. How often should I check my credit report?

You can check your credit reports regularly. Free weekly online credit reports are available from the three major bureaus through AnnualCreditReport.com.

Leave a Reply